V. The Only Structural Defense

Every major collateral failure since 2024 exploited the same missing controls. Slow reporting. Borrower supplied evidence. Weak entity resolution. Weak lien visibility. Weak cash confirmation. No cross program duplicate detection. The failures were different in surface details but consistent in operating logic. That consistency matters because it turns post mortems into product requirements. The market no longer needs a general warning about fraud. It needs a control architecture that answers the same questions before every purchase.

Before capital buys the asset, can the claim be independently resolved, legally cleared, cash traced, and cross checked for uniqueness?

Ledger, legal, cash, collision.

Four control domains govern asset integrity.

The control architecture collapses into four domains. Ledger asks whether the receivable exists, matches the buyer record, and clears approval logic. Legal asks whether the claim is encumbered, mistitled, or attached to the wrong entity. Cash asks whether the payment path, bank account, and remittance pattern validate the asset. Collision asks whether the same claim, or a materially identical claim, already sits inside another program.

At minimum the system now runs onboarding lien search, continuous UCC monitoring, supplier-side ERP forensics, remittance routing checks, and supplier attestations before capital buys the asset.

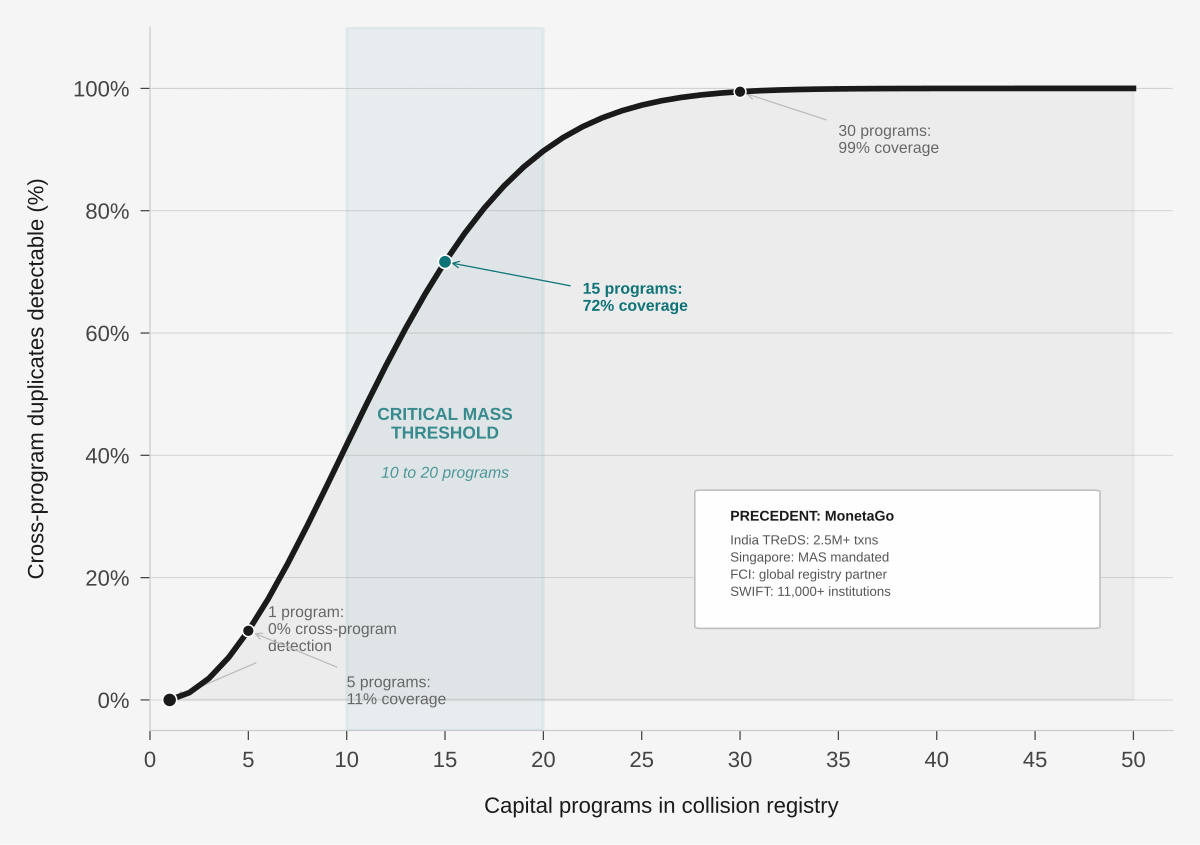

Cross program visibility is the missing control.

A collision registry changes the geometry of the problem.

The market has no shared duplicate detection layer. That is why every lender can be correct inside its own file and wrong at the portfolio level. A collision registry changes the geometry of the problem. With one program there is no cross program visibility. With many programs, detection coverage compounds quickly. Once the network reaches critical mass, duplicate claims become harder to finance than to originate.

This is the difference between periodic auditing and market level uniqueness control. The first finds losses after the fact. The second blocks the asset before funding.

Sources: DOJ indictments, FCA enforcement proceedings, court filings, UCC Article 9, OFAC lists, MINT architecture.