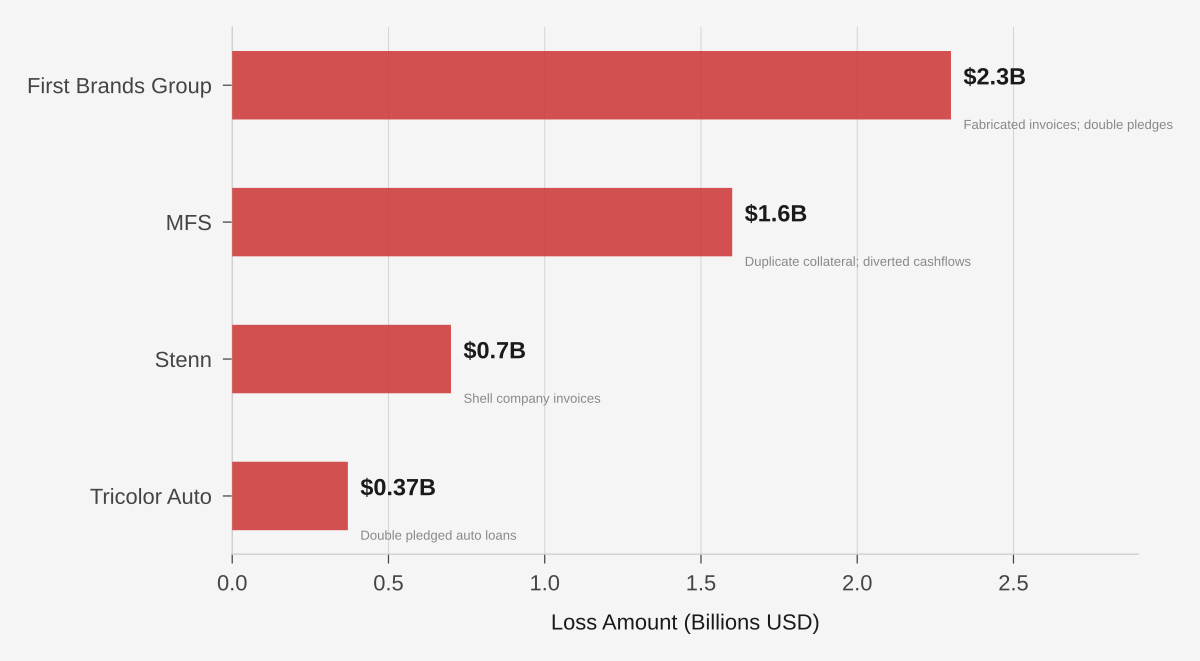

I. $5B in Eighteen Months

Late 2025 and early 2026 ended the fiction that collateral verification was a back office nuisance. Four separate failures surfaced through fabricated invoices, duplicate collateral, falsified portfolio data, or diverted cash. The common feature was not ordinary credit deterioration. It was operational deception inside slow, bilateral control systems. More than five billion surfaced across First Brands, MFS, Stenn, and Tricolor in eighteen months. Then the same market that financed those assets gated liquidity. Fraud arrived first. Repricing followed.

First Brands: $2.3 billion in forged receivables, multiple duplicate pledges, $1.9 billion not remitted to lenders. MFS: £930 million plus shortfall, connected borrowers, duplicate collateral, diverted income streams. Stenn: $700 million plus hole, shell company invoices mimicking blue chip buyers, roughly 10 percent recovery. Tricolor: $370 million plus, falsified portfolio data, duplicate auto loan pledges across lenders.

Sources: Bloomberg, Reuters, DOJ indictments, FCA enforcement proceedings, court filings.

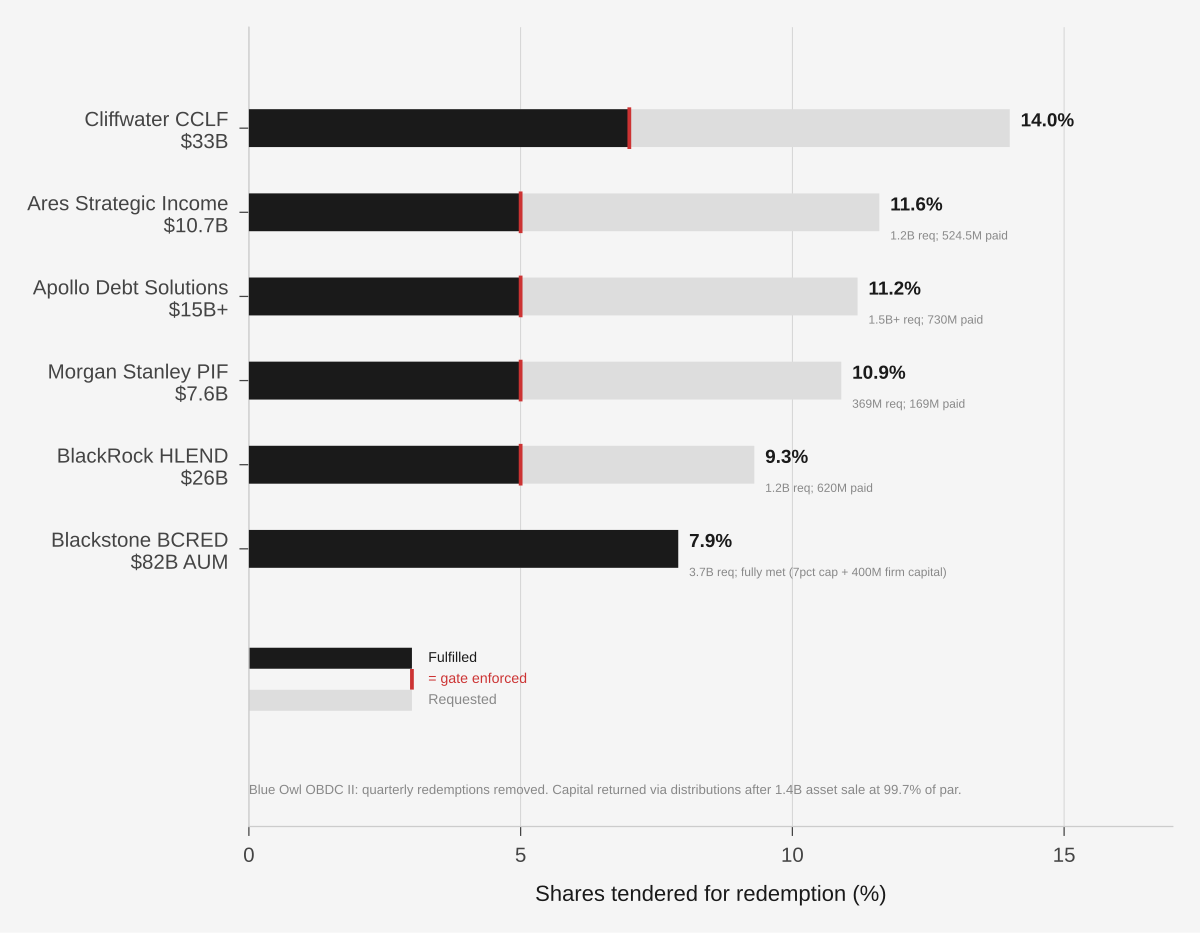

Semi liquid structures stopped acting liquid.

Redemption gates exposed the liquidity mismatch.

Once the fraud cycle reached the market, investor cash stopped moving as advertised. More than $150 billion across major retail private credit vehicles hit withdrawal limits in Q1 2026. The important point is not retail sentiment. It is structure. These vehicles promised periodic liquidity against portfolios whose underlying assets were already showing stress, opacity, and concentrated sector exposure. When redemption pressure arrived, the gates showed what the market already knew: the collateral stack was being repriced faster than managers could sell or certify it.

Goldman Sachs projected $45 to $70 billion of asset shrinkage over two years. More than $4.6 billion remained trapped behind withdrawal limits.

Sources: Goldman Sachs, Bloomberg, company letters, SEC filings.

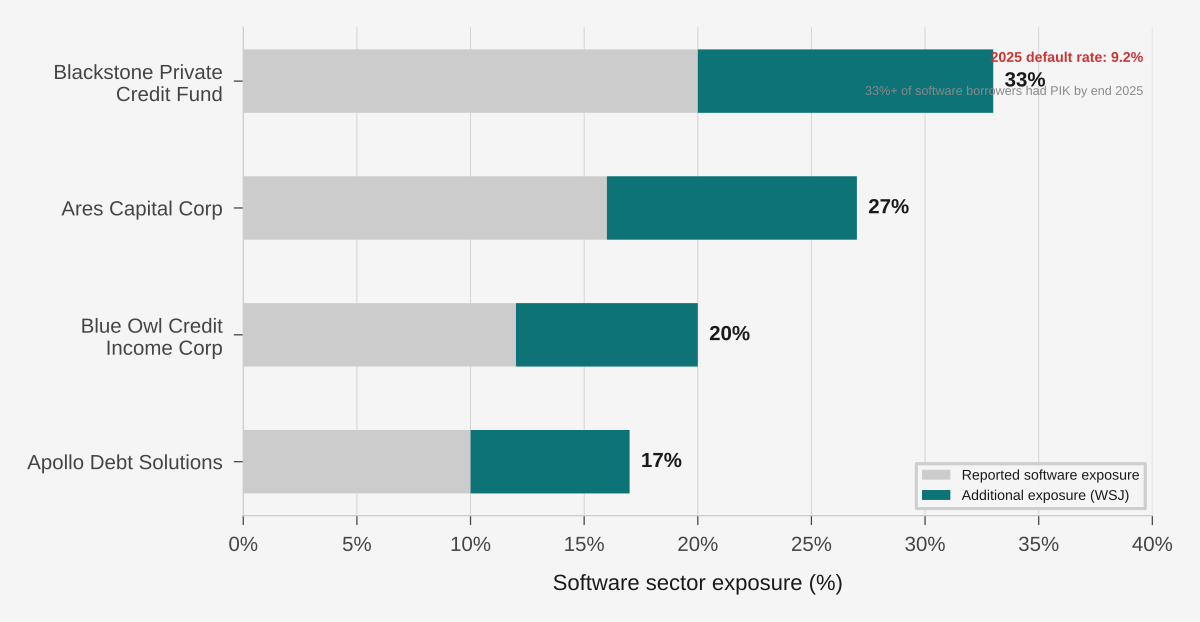

The gated funds owned the same stress.

Hidden concentration, weaker cash interest, and illiquidity surfaced together.

Public reporting exposed a second layer of fragility. Several of the largest retail private credit funds carried materially more software exposure than public filings implied. The same group, Blue Owl, Blackstone, Ares, Apollo, also appeared in the gating cycle. Fitch put the United States private credit default rate at 9.2 percent for full year 2025, a record. Reuters then reported that more than a third of software borrower agreements included payment in kind options by the end of 2025. Hidden concentration, weaker cash interest, and gated liquidity all showed up together.

This was not a narrow sector problem. It was a disclosure problem, a control problem, and a liquidity problem at the same time.

Sources: Wall Street Journal, Reuters, Fitch.